🏢 Demystifying Bank Loan Tenure & LTV Eligibility in Singapore (A Quick & Simple Guide!)

If you are planning to finance your dream home or your next investment property, understanding the rules around Bank Loan Tenure and Loan-To-Value (LTV) limits is absolutely critical. The Monetary Authority of Singapore (MAS) set out specific guidelines (effective since 6 July 2018) that dictate exactly how much banks are allowed to lend you based on your age and loan duration.

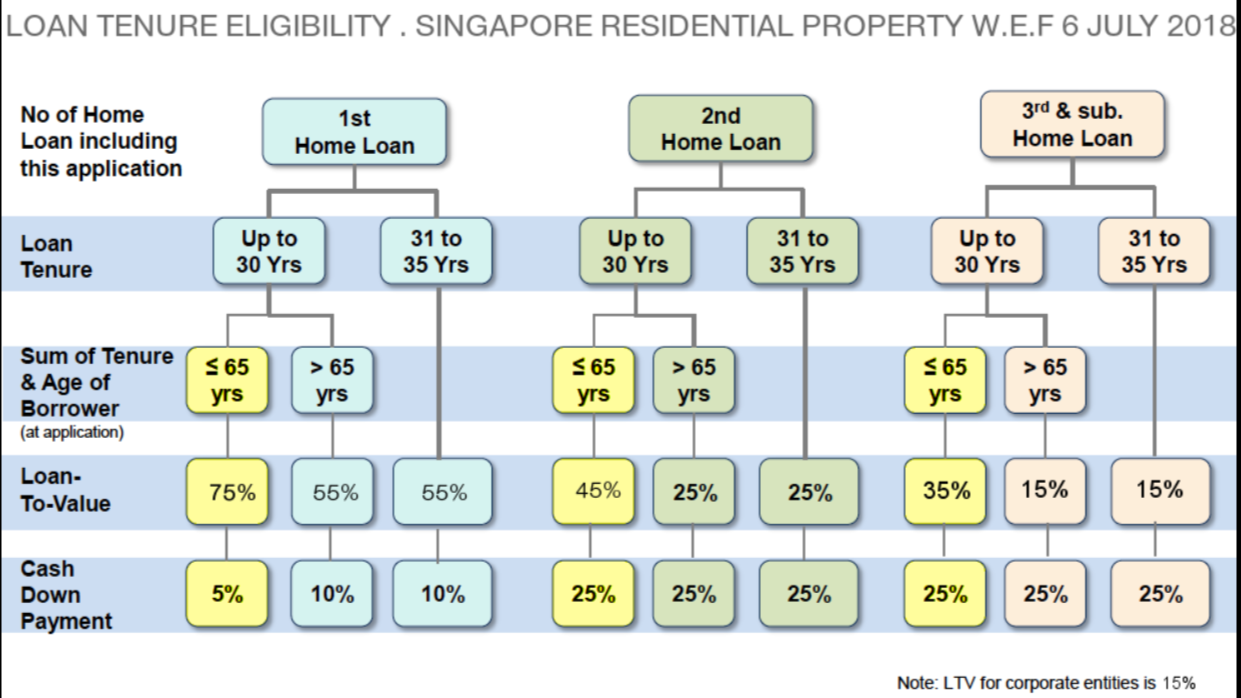

To save you the headache of deciphering complicated financial jargon from the Bank Loan Tenure Eligibility Chart, I’ve broken down everything you need to know into a simple, easy-to-understand pointer format!

🔹 1. The Absolute Maximum Loan Tenures

First things first, there is a hard cap on how long your mortgage can be:

For Private Properties (Condos, Landed): The maximum loan tenure is 35 years.

For HDB Flats: The maximum loan tenure is 30 years.

🔹 2. The "Golden Rules" for Maximum Loan (75% LTV)

For your first property loan, the bank can lend you a maximum of 75% of the property’s purchase price or valuation (whichever is lower). However, to qualify for this full 75%, you must meet both of these conditions:

Tenure Limit: Your loan tenure must not exceed 30 years (for Private) or 25 years (for HDB).

Age Limit: The loan tenure plus your current age must not extend past the age of 65. (Example: If you are 40 years old today, your maximum tenure to get a 75% loan is 25 years).

🔹 3. What Happens If You Exceed the Limits?

If you choose to stretch your loan beyond 30 years (Private) / 25 years (HDB), OR if the loan tenure extends beyond your 65th birthday, your borrowing limit drops significantly:

Your LTV limit drops from 75% down to 55%.

The Cash Impact: For a 75% LTV loan, your minimum pure cash downpayment is 5%. But if your LTV drops to 55%, your minimum pure cash requirement doubles to 10%.

🔹 4. Buying a 2nd or 3rd Property?

If you currently have outstanding housing loans, the financing rules get much tighter to prevent over-leveraging:

2nd Housing Loan: Your maximum LTV drops to 45% (and plunges to 25% if you break the tenure/age limits mentioned above).

3rd Housing Loan (and beyond): Your maximum LTV drops to 35% (and plunges to 15% if you break the tenure/age limits).

💡 Let's Look at the Bigger Picture!

Navigating the Singapore real estate landscape goes way beyond simply picking a New Launch or hunting down a Resale property. Real estate is about holistic wealth creation, and making the wrong financing move can cost you heavily.

Are you looking for expert advice on other real estate matters? Whether you need help with:

Strategic Financial Planning & Mortgage Structuring (Ensuring you don't overpay on cash downpayments)

Property Portfolio Restructuring & Asset Progression

Navigating Complex ABSD/TDSR/LTV Regulations

Leasing, Tenancy Management, and Maximizing Rental Yields

...I’ve got you covered!

📞 Don't leave your real estate journey to guesswork. Contact me today! Let’s grab a coffee and tailor a comprehensive property strategy that works specifically for your financial goals.